Let’s be honest: when most people hear the word budget, they picture spreadsheets, guilt, and restriction. But budgeting isn’t about saying “no” to everything you enjoy—it’s about giving every dollar a job so you can spend with confidence.

Whether you want to pay down debt, build savings, or just feel more in control of your finances, a solid budget is a great place to start.

Step 1: Know Where Your Current Money Is Going

Before you can build a budget, you need to understand your current spending. Use apps like our Financial Life Organizer (free) or Monarch Money (paid, but 7 day free trial) to connect your bank and credit card accounts and review your current expenses. Group your expenses into categories like housing, groceries, eating out, subscriptions, and travel.

This helps you spot patterns, areas where you might be overspending, and opportunities to reallocate money toward your goals.

Step 2: Plan How You Want to Spend Your Money

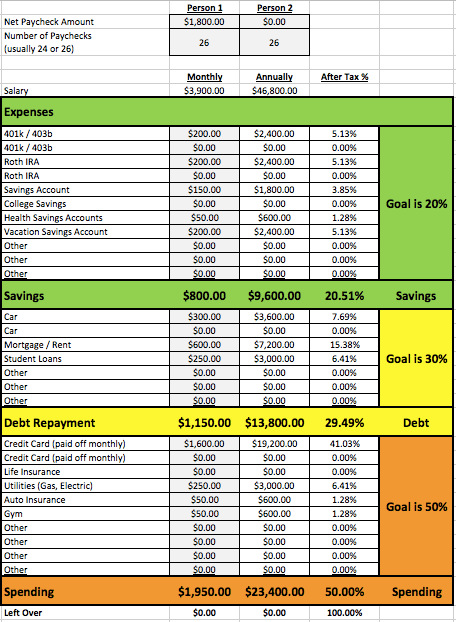

I am a fan of the “20/30/50” budget. It’s straightforward and allows you to spend on the things you love, while still keeping your spending in line with your savings. The key is finding what you value and enjoy spending your money on. For example, if you value a nice house, you can spend more on a house, but it might come at a cost of nicer cars or vacations. Let’s look at how this budget is set up and how it can help you plan and stick with it.

The “20” = 20% in Savings: The first step in the budgeting process is to take 20% of your after-tax income and save it. At least 10% should be going towards your retirement (Roth IRA, 403b or 401k account). If you want to have a rich life in the future, plain and simple, you have to adjust your spending today to pay for it. The longer you delay and put this lifestyle change into effect, the harder it gets to try and take money from your current expenses due to “lifestyle creep” (aka, make more, spend more).

The savings category is where you save for your future self. Common ways to save here are a standard savings account, Roth IRA, 403b, 401k, Health Savings Account (HSA), 529 College Savings Accounts, Vacation account, Home Improvement account, Wedding account, etc.

The “30” = 30% Debt Repayment: This category can make the biggest difference in your budget. If your debt is too high, it robs you from saving for your future self or spending and having a nice lifestyle right now. You should not have any credit card debt, but if you do, eliminating it early should be your top priority as it can have devastating interest rates – sometimes well over 20% – which can be very difficult to dig out from under.

This is where you pay for your past spending decisions. Common expenses in this category are auto loans or leases, student loans, mortgages or rent, etc.

The “50” = 50% Spending: This is the category where all the rest of your spending goes. Since most of us put everything on a credit card each month (hopefully you’re earning rewards points through a credit card program, but paying it off in full each month), you should look at your average credit card bill to see where the money is going. Do not forget to add in other expenses paid directly from your checking account and non-monthly bills such as utilities, life insurance, or car insurance. The fewer costs you have in this category, the more progress you’ll make paying down debt and saving for your future self.

This is where you pay for your current spending decisions. Common expenses in this category are your credit card balances, utilities, health insurance, gym, cell phone bills, auto insurance, life insurance, etc.

The “20/30/50” budget is designed to set you up for future success by saving for retirement, paying off debt, and enforcing good life-long budgeting habits. More importantly, it’s set up to help you spend money on what you value.

When Rebecca and I sat down and did our budget we settled at 25% (Savings) /30% (Debt Repayment) /45% (Spending) – again, cutting down our spending now so we can enjoy a long life of fun later.

Step 3: Use Tools to Make Monitoring Your Spending Easier

Did you know that spending decreased by 15.7% on average for those who downloaded and used a financial app. If keeping track of every expense sounds overwhelming, don’t worry—there are tools that can do the heavy lifting for you. Apps like our Financial Life Organizer or Monarch Money to connect to your accounts, track spending automatically, and help you stay on top of your goals.

How I manage our budget - I used the budget spreadsheet to develop our spending plan and now use Monarch Money to monitor our day-to-day spending. This helps me notice what we are spending money on and if we spent a lot or a little in each category for the month. For example, we would like to spend no more than $1,000 a month on dining out, so when I see that we have only spent $600 with one week left, I know it is ok to go to a nice restaurant. Conversely, if I see that I have already spent $1,250, we should wait until next month.

Step 4: Make Your Budget a Living Document

Your budget isn’t set in stone. Review it regularly—especially after big life changes like moving, getting a raise, or starting a family. The goal is progress, not perfection.

If you overspend one month, don’t beat yourself up. Adjust and keep moving forward.

Final Thoughts: A Budget Is a Plan for Your Future

Budgeting isn’t about restriction—it’s about freedom. The freedom to say yes to the things that matter most. The freedom to stop worrying about money and start making progress.

If you want help creating a budget or integrating it into a full financial plan, we’re here for you. Schedule a meeting and let’s talk about what’s possible.