When you retire from the New York State Teachers’ Retirement System (NYSTRS), one of the most important decisions you’ll make is how your pension benefit will be paid for the rest of your life. You must choose one payment option on your retirement application.

Your decision should be based on factors such as:

Your family’s financial needs and long-term goals

Other sources of retirement income (like savings and investments)

Your age and health at retirement

There isn’t a “one-size-fits-all” best option — what’s right for you depends on your personal situation. Talk with your family, a financial advisor, and a NYSTRS representative before making your selection.

Your Pension Payment Choices

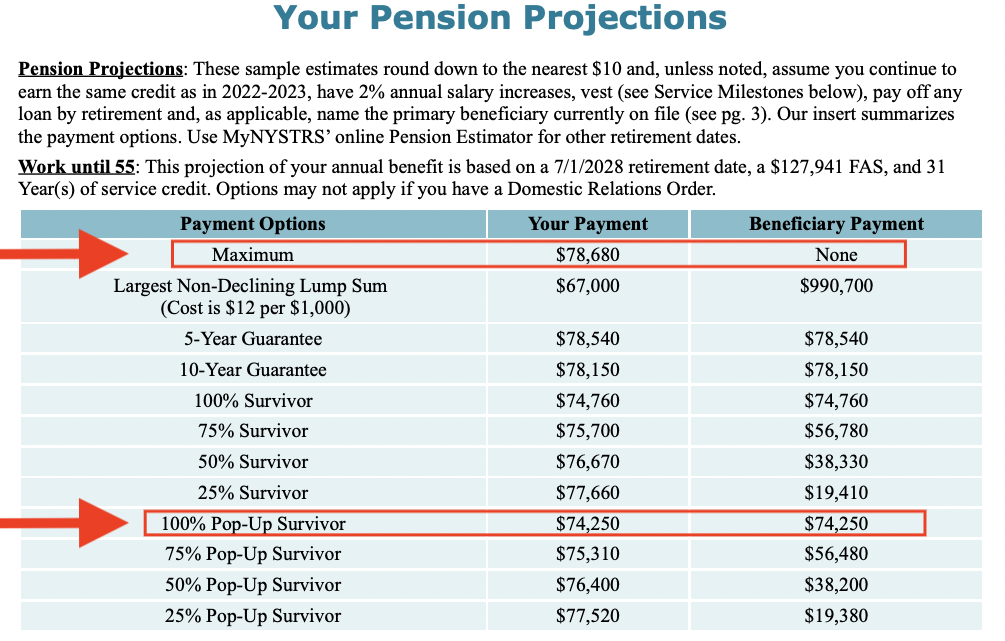

1. Maximum Benefit (Single Life Allowance)

This option gives you the highest monthly payment for life. However:

Payments stop when you die — no ongoing benefit goes to a spouse or beneficiary.

(Tier 2–6 members may still qualify for a one-time Paragraph 2 death benefit, but this is separate from the monthly pension payments.)

Best for you if:

You are single or have no dependents.

Your spouse or beneficiaries don’t need income from your pension.

You already have enough life insurance or other assets to protect loved ones.

2. Pop-Up Survivor (Joint) Benefit Option

If you want to provide income to a spouse after you die, you can choose a pop-up survivor option. These pay a lowermonthly pension during your lifetime in exchange for continuing payments to your beneficiary after your death.

Key features:

You name one beneficiary and can’t change them after the 30-day post-retirement window.

Your monthly benefit is smaller than the Maximum, and it’s calculated based on your age and your beneficiary’s age.

If your beneficiary dies before you, your pension payment goes back up to the Maximum amount.

Most people choose this if:

They want to ensure lifetime income for a spouse.

They don’t have enough private life insurance to protect their family.

What Does This Really Look Like?

In this example a teacher’s Maximum pension would be $78,680 per year. If that teacher wants to guarantee lifetime income for a spouse, choosing a survivor option could reduce their benefit to $74,250 per year. That means they’re essentially “buying” the survivor benefit for $4,430 a year — less money during life in exchange for financial protection for their spouse.

The Process

You can receive benefit payment estimates at a consultation with a NYSTRS representative, by using the Pension Estimator in the MyNYSTRS’ website, or by requesting benefit projections be mailed to you (call 800.348.7298 Ext. 6020). In all cases, provide the following information:

Retirement date(s). Request estimates for different dates to see how much your benefit increases if you continue to work.

Current and future salaries, including additional earnings (e.g., summer school, coaching, etc.). If you do not know your salaries, we will assume 2% increases per year over the last known salary.

The date of birth and gender of your beneficiary for estimates of the survivor options that guarantee a lifetime income for one beneficiary.

Review all sources of income and research your eligibility for (and the cost of) private life insurance. If another person is dependent on your income, determine what he/she will need to live comfortably should you predecease him/her.

File your retirement application with NYSTRS. (Resigning from your employer does not automatically trigger your retirement from NYSTRS and the payment of your benefit.) Complete your retirement application online in MyNYSTRS (age 55+) or submit a paper application (RET-54). Be sure to select the benefit payment choice that best meets your needs and those of your beneficiary.

You may change, if necessary, the benefit payment you selected at retirement up to 30 days after your date of retirement. To do so, complete and file with NYSTRS the Election of Retirement Benefit (RET-54.6) form.

Our Recommendation

If you are married, we often recommend the 100% pop-up survivor option. You’ve spent a career earning this pension, and this choice helps make sure it continues to benefit your family. Because payments last for both your lifetime and your spouse’s lifetime, this option increases the likelihood of long-term income from your pension.